Value Added Tax (VAT) in Switzerland is an indirect consumption tax levied by the federal government. Governed by the Swiss VAT Act (MWSTG / LTVA), it applies to supplies of goods and services provided on Swiss territory, as well as to imports of goods.

Since 1 January 2024, the rates have been adjusted following the AVS 21 reform aimed at financing the old-age and survivors’ insurance (OASI). The standard rate rose from 7.7% to 8.1%, the reduced rate from 2.5% to 2.6%, and the special accommodation rate from 3.7% to 3.8%. These rates remain in force in 2026.

This guide details how the Swiss VAT system works, the VAT registration obligations with the Swiss Federal Tax Administration, the input tax deduction mechanism, as well as the VAT return methods, invoicing, and management of tax obligations. To understand how VAT fits into the broader tax landscape, see our guide on taxation in Switzerland.

📑 Table of Contents

How does VAT work in Switzerland? (Basic principles)

The Swiss VAT system is based on the principle of neutrality: the tax must be borne by the final consumer and must not constitute a burden for the registered businesses that intervene in the supply chain.

A federal indirect tax

Unlike other Swiss taxes that are shared between the Confederation, cantons, and municipalities, VAT is an exclusively federal tax. The revenue feeds the federal budget and, since 2024, contributes to the financing of OASI (old-age and survivors’ insurance).

According to the Swiss Federal Tax Administration (FTA) and the Swiss VAT Act (MWSTG / LTVA), the FTA is the competent authority for:

- VAT registration of taxable persons in the register of VAT taxpayers

- Checking returns and periodic VAT filings

- Collecting amounts due

- Refunding deductible VAT

Principle of territoriality

Under Swiss federal legislation, the following are taxable:

- Supplies of goods and services provided for consideration on Swiss territory

- Imports of goods into Switzerland

- The acquisition of services supplied by entities established in other countries

The place of supply determines liability to Swiss VAT. For services, specific rules apply depending on the nature of the supply and the status of the recipient (taxable person or non-taxable person).

Multi-stage collection mechanism

At each stage of the production and distribution chain:

- The taxable person invoices VAT to its customers when selling goods or services (output VAT)

- The taxable person deducts the VAT paid on its business purchases (input tax)

- The taxable person remits to the tax authority the difference between output VAT and input tax

This mechanism ensures that only the value added at each stage is actually taxed, thus avoiding cascading taxation.

What are the Swiss VAT rates in 2026?

Switzerland applies three distinct VAT rates, set by the Federal Constitution and enacted in legislation. These rates have been in force since 1 January 2024 and remain so in 2026. The Swiss VAT rates are set by the Swiss Federal Tax Administration (FTA).

Standard rate: 8.1%

The standard rate of 8.1% applies to the majority of supplies of goods and services that are not expressly subject to the reduced rate or the special rate.

Examples of supplies at the standard rate:

- Sale of manufactured goods (electronics, clothing, furniture)

- Professional services (consulting, expertise, engineering)

- Repair and maintenance services

- Restaurant services (excluding accommodation)

- Digital transactions (e-commerce, software, SaaS)

Reduced rate: 2.6%

The reduced rate of 2.6% applies to essential goods and certain key services, in accordance with federal regulations.

Categories concerned:

- Foodstuffs (bread, milk, fruit, vegetables, meat)

- Medicines (prescription and non-prescription)

- Newspapers, magazines and books (paper and electronic formats)

- Animal feed

- Seeds, plants and flowers (agricultural use)

⚠️ Important note

Correct invoicing requires precise classification. For example, an alcoholic beverage is subject to the standard rate, while a fruit juice falls under the reduced rate. A specialised Corporate Services Provider can assist you with the proper management and classification of your transactions.

Special accommodation rate: 3.8%

The special rate of 3.8% applies exclusively to services in the accommodation sector, in accordance with federal regulations.

Supplies concerned:

- Hotel stays

- Accommodation in inns, motels and campsites

- Rental of furnished rooms (temporary stays)

Exclusions: Restaurant services, breakfasts included in the room price, or other ancillary services remain subject to the standard rate of 8.1%.

Summary table of Swiss VAT rates 2026

| Category | Applicable rate | Examples of supplies |

|---|---|---|

| Standard rate | 8.1% | General goods, professional services, e-commerce, restaurant services |

| Reduced rate | 2.6% | Foodstuffs, medicines, books, newspapers, animal feed |

| Special rate | 3.8% | Hotel accommodation, overnight stays, camping (excluding restaurant services) |

Swiss VAT rates applicable since 1 January 2024 (source: Swiss VAT Act, FTA).

Who has to register for VAT in Switzerland?

VAT registration in Switzerland is determined by the taxable turnover generated and the nature of the activity carried out. The legislation distinguishes between mandatory and voluntary registration.

VAT registration threshold: CHF 100,000

Under federal regulations, the following are mandatorily liable for Swiss VAT:

- Any business whose worldwide taxable turnover from taxable supplies exceeds CHF 100,000 over 12 months

- This threshold applies to worldwide turnover, not solely to sales made in Switzerland

⚠️ Key rule for foreign businesses

A company established in another country with a worldwide turnover of CHF 500,000 but only CHF 5,000 generated in Switzerland is liable from the very first franc of taxable supply on Swiss territory. VAT registration with the tax authority becomes mandatory.

Voluntary registration

Entities whose taxable turnover is below CHF 100,000 may opt for voluntary registration in order to:

- Recover input tax on their business purchases

- Facilitate transactions with other registered businesses

- Enhance their image of professional compliance

Voluntary registration commits the entity for a minimum period of 3 years.

Registration procedure

VAT registration is completed via the tax authority’s online portal:

- Create an account on the online portal

- Complete the registration form (IDE number, activity, estimated turnover)

- Submit supporting documents (commercial register extract, articles of association)

- Validation and assignment of a VAT number (format: CHE-xxx.xxx.xxx MWST)

- Processing time: generally 2 to 6 weeks

From the date of VAT registration, the taxable person must:

- Issue compliant invoices including VAT on taxable supplies

- Submit periodic VAT returns

- Meet payment and filing deadlines

Swiss VAT for foreign businesses and exporters

Companies established in other countries are subject to specific VAT liability rules depending on the nature of their supplies in Switzerland and their organisational structure.

Foreign businesses without a permanent establishment

An entity based in another country making taxable supplies in Switzerland without having a permanent establishment there must, under federal legislation:

- Proceed with VAT registration with the tax authority as soon as the threshold of CHF 100,000 in worldwide turnover is crossed

- Appoint a fiscal representative domiciled in Switzerland who will assume the tax obligations

- Submit periodic VAT returns through this representative

The registration process for non-residents is detailed in our article on the fiscal representative in Switzerland.

Exports

Exports of goods from Switzerland are zero-rated, in accordance with regulations. To benefit from this zero-rating, the taxable person must:

- Provide proof of export (customs documents, proof of departure from Swiss territory)

- Retain supporting documents for 10 years

- Expressly indicate on the invoice that the supply is zero-rated (0%)

Example: French company selling to a Swiss customer

Situation: A French company (worldwide turnover EUR 500,000) sells industrial machinery to a Swiss customer for CHF 80,000.

Application:

- The company exceeds the threshold of CHF 100,000 worldwide taxable turnover

- It must register for Swiss VAT and appoint a fiscal representative

- If the goods are delivered in Switzerland: VAT at 8.1% is charged

- If the goods are zero-rated exports leaving Switzerland: exemption possible subject to conditions

Digital services and e-commerce

Electronic services (SaaS, streaming, online courses) provided to Swiss customers by companies established in other countries are taxable in Switzerland if the recipient is established in Switzerland.

To secure your compliance and Swiss VAT management, call on our VAT fiscal representation service in Switzerland.

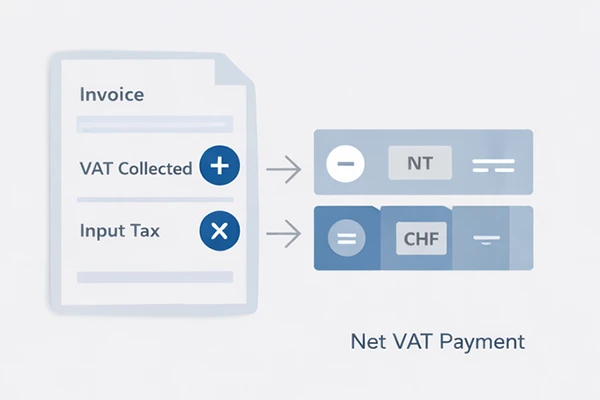

Input tax deduction mechanism

The system for deducting upstream VAT is a fundamental pillar of the Swiss tax mechanism. It guarantees the neutrality of the tax for registered businesses.

Definition of input tax

Input tax refers to the VAT charged to a taxable person on:

- Purchases of goods and services necessary for its taxable activity

- Imports of goods

- Acquisition of services from suppliers established in other countries

The taxable person may deduct this input tax from the VAT it collects on its own sales, provided the expenditure is related to an activity giving entitlement to deduction.

Calculation: output VAT – input tax

The amount payable to the tax authority (or refundable) is calculated as follows:

VAT due = Output VAT − Input tax

Simulation of a sales cycle

Company Sàrl: Furniture manufacturer

Quarterly transactions:

- Purchases of wood and supplies: CHF 50,000 excl. VAT → VAT 8.1% = CHF 4,050 (input tax)

- Furniture sales: CHF 120,000 excl. VAT → VAT 8.1% = CHF 9,720 (output VAT)

VAT return calculation:

- Output VAT: CHF 9,720

- Input tax: CHF 4,050

- Amount payable: CHF 5,670

Conditions for deduction

The deduction of upstream VAT is subject to strict conditions:

- Link with taxable activity: Expenditure must be incurred in the context of supplies giving entitlement to deduction

- Valid supporting documents: Compliant invoices mentioning the supplier’s VAT number

- Retention: All documents must be archived for 10 years

Reduction of the right to deduct

If a company carries out both supplies giving entitlement to deduction (taxable) and supplies excluded from the scope of VAT, it must apply a proportional reduction of the right to deduct in accordance with federal regulations.

Swiss VAT returns and reporting methods

Federal legislation provides for several VAT filing methods, adapted to different types of activities and structures.

Effective method (standard method)

The effective method constitutes the reference method. It consists of:

- Calculating output VAT on all taxable supplies

- Deducting input tax on business purchases

- Declaring the net amount to the tax authority

This method requires rigorous accounting management and precise tracking of all transactions.

Net tax debt rate method (NTDR)

The net tax debt rate (NTDR) method simplifies VAT filing for SMEs.

Principle: Instead of precisely calculating deductible input tax, the taxable person applies a flat-rate percentage set by the tax authority according to the sector of activity.

Access conditions:

- Annual taxable turnover < CHF 5,024,000 (2026 threshold)

- Eligible activity according to the list of sectors defined by the authority

Advantages:

- Considerable administrative simplification

- No need to itemise input tax transaction by transaction

- Time savings for smaller structures

Filing frequency

VAT returns must be submitted to the tax authority according to a set frequency:

| Annual turnover | Filing frequency | Submission deadline |

|---|---|---|

| > CHF 5,024,000 | Quarterly | 60 days after the end of the quarter |

| < CHF 5,024,000 | Semi-annual (default) | 60 days after the end of the semester |

| On request | Annual (if below threshold and good compliance history) | 60 days after the end of the financial year |

Swiss VAT return frequencies and deadlines (source: federal legislation).

Using the ePortal

Since 2022, all VAT filings must be completed electronically via the tax authority’s online portal. This system allows:

- Secure submission of VAT returns

- Electronic payment of amounts due

- Viewing the history of filings

- Receipt of official notifications

💡 RISTER Tip — Corporate Services Provider Geneva

Failure to meet filing and payment deadlines automatically triggers default interest (4% per year) and reminders. A specialised Corporate Services Provider like RISTER ensures rigorous management of your obligations and the compliance of your VAT returns.

Special cases

SaaS and digital services

Electronic services (Software as a Service, online training, streaming) provided by companies established in other countries to Swiss customers are taxable in Switzerland under the principle of the place of the recipient.

If the recipient is a Swiss taxable person, they must self-assess the VAT (acquisition tax). If the recipient is a private individual, the supplier established in another country must register for Swiss VAT.

E-commerce and online sales

Online sellers based in other countries (marketplaces, e-commerce stores) must register for Swiss VAT once their worldwide taxable turnover exceeds CHF 100,000, even if sales of goods in Switzerland are minimal.

Since 2025, electronic platforms are required to declare and pay VAT for sales of goods made by third-party sellers, bringing Switzerland in line with European reforms.

Donations and subsidies

Donations and subsidies are generally outside the scope of VAT as they do not constitute consideration for a supply. However, if a supply is provided in exchange (sponsorship), VAT may apply and must appear on the invoice.

Deregistration from the VAT register

An entity may request deregistration from the register of taxable persons if:

- Its taxable turnover durably falls below the threshold of CHF 100,000

- It permanently ceases its taxable activity

Deregistration triggers the obligation to repay the input tax deducted on goods and services not yet used (input tax correction).

FAQ: Your questions about VAT in Switzerland

Why did the Swiss VAT rate increase to 8.1%?

Answer: The increase in the standard rate from 7.7% to 8.1% results from the AVS 21 reform, adopted in a popular vote on 25 September 2022. This rise of 0.4 percentage points is intended to finance old-age and survivors’ insurance (OASI) in the face of demographic ageing. The reduced (2.6%) and special (3.8%) rates were also adjusted proportionally. These rates came into force on 1 January 2024 and remain applicable in 2026.

How do I get a VAT number in Switzerland (IDE)?

Answer: VAT registration is completed via the tax authority’s online portal:

- Create an account on the online portal

- Complete the registration form with your IDE number (unique business identifier)

- Provide supporting documents (commercial register extract, articles of association, description of activity)

- The authority validates your application and assigns a VAT number (format: CHE-xxx.xxx.xxx MWST)

- Processing time: 2 to 6 weeks on average

Companies established in other countries must mandatorily appoint a representative domiciled in Switzerland to carry out this process.

What is the net tax debt rate method?

Answer: The net tax debt rate (NTDR) method is a simplified VAT filing option reserved for SMEs with annual taxable turnover below CHF 5,024,000. Instead of precisely calculating input tax on each transaction, the taxable person applies a flat-rate percentage set by sector of activity. This method considerably reduces the administrative burden and simplifies management, but does not always allow optimal recovery of input tax. A Corporate Services Provider can help you determine which method is most advantageous for your activity.

Is VAT due on digital services?

Answer: Yes. Electronic services (SaaS, online training, streaming, downloads) provided to Swiss customers are taxable in Switzerland under the principle of the place of the recipient. If the recipient is a registered taxable person, they self-assess the VAT (acquisition tax). If the recipient is a private individual, the supplier established in another country must register for Swiss VAT once its worldwide taxable turnover exceeds CHF 100,000 and appoint a representative in Switzerland.

How do I invoice a Swiss customer from France without VAT?

Answer: To invoice a Swiss customer without French VAT, you must prove that the transaction constitutes an export outside the EU. Conditions:

- Retain proof of export (customs documents, proof of departure from French territory)

- State on the invoice: “VAT exempt – Export outside the EU – Article 262 I CGI”

- The Swiss customer will pay Swiss VAT (8.1%) upon importing the goods into Switzerland

If your French company exceeds CHF 100,000 in worldwide turnover and makes taxable supplies in Switzerland, you will also need to register for Swiss VAT and appoint a fiscal representative.

Is a fiscal representative liable for their client’s debts?

Answer: Yes. Under federal regulations, the representative appointed by a company established in another country bears joint and several liability for the VAT debts of their principal. This means the tax authority can claim payment of amounts owed directly from the representative if the foreign company fails to meet its obligations. This is why Corporate Services Provider generally require a bank guarantee or security deposit before accepting a representation mandate. RISTER, as a specialised Corporate Services Provide, rigorously assesses each case to secure this compliance.

Sources

This guide was written based on the following official sources:

Swiss legislation:

- Swiss VAT Act (MWSTG / LTVA) – RS 641.20

- VAT Ordinance (MWSTV / OTVA) – RS 641.201

- Federal Constitution – Art. 130 (OASI financing)

Swiss authorities:

- Swiss Federal Tax Administration (FTA) – www.estv.admin.ch

- Official publications and VAT directives

- Electronic portal for taxable persons

Recent reforms:

- AVS 21 Reform – New Swiss VAT rates from 1 January 2024

- Legislative amendment – E-commerce platforms (2025)

- Net tax debt rates – 2026 thresholds